Valuation

Valuation methods for start-up companies.

How much is my startup worth?

As an entrepreneur, you may be looking for venture capital (VC) to help fund your start-up. Before you can approach potential investors, you need to know how to valuate your start-up. It is important to know which valuation method to use; there are different methods to value early-stage startups and late-stage startups. In this article, we will explain the process of start-up valuation and provide some tips on how to do it.

The process of valuation is important not only for entrepreneurs seeking VC but also for anyone looking to buy or sell a start-up. By understanding how to value a start-up, you will be able to make more informed decisions about your business.

In this article, we will take a look at the different methods of valuating start-ups and the factors that you need to consider in each case. How much fund you will raise and how much of your company you will give up in the process will depend on your valuation.

The stage of your company will be important in the method to use. If your company is already generating significant revenue, you may prefer an analytical approach such as discounted cash flow valuation method. As you can observe the public traded companies in the stock market; the valuation of a company is most determined by numeric factors such as EBITDA, revenues, free cash flow etc.

How pre-revenue startups can be valued is a different approach. If your company is pre-revenue or in early stages you may seek to prefer a method that would focus more on abstract values such as Berkus Method.

It shouldn’t discourage you if your startup is at an early stage and you can’t rely on concrete financial analysis. According to an article published in Harvard Business Review in 2021:

“Few VCs use standard financial-analysis techniques to assess deals. The most used metric is the cash returned from the deal as a multiple of the cash invested.” https://hbr.org/2021/03/how-venture-capitalists-make-decisions

Before diving into the different startup valuation methods, please keep in mind that factors such of intellectual property on startup value or the tangible assets are not taken into consideration. You would need to reflect all critical factors that might affect your valuation into your model.

DCFV Discounted Cash Flow Model:

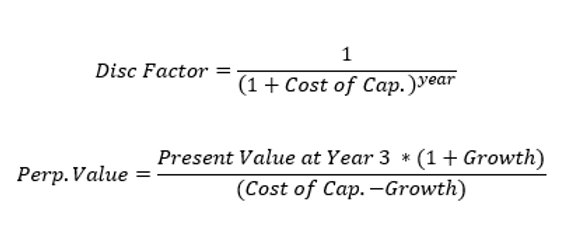

The Discounted Cash Flow Valuation model analyzes how much money the startup expects to generate in the future and discounts the value of future cash to this day. Money in your pocket today is more valuable than money you will get 5 years from now, time value of money is an important concept that you need to understand while dealing with valuation.

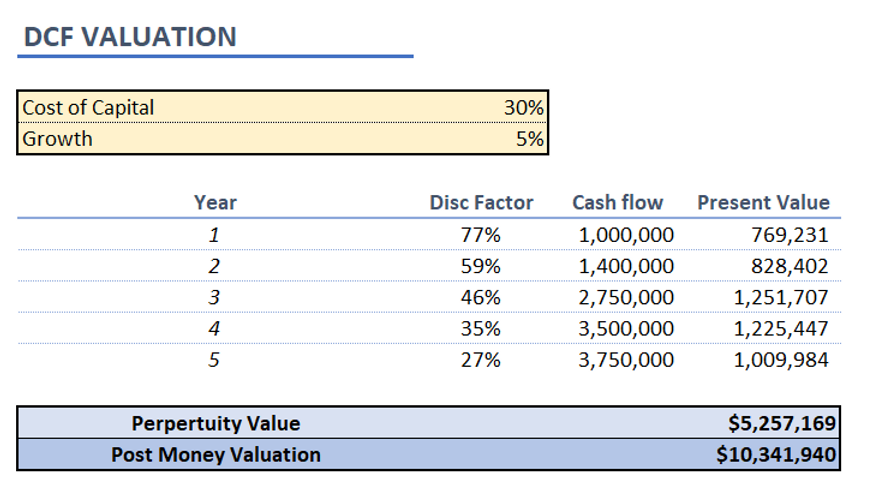

In the example below the company presents 5 year net cash flow. The cost of capital (used for discount factor) and company growth factors are assumed at 30% and 5%. The 5 year present values of company cash flow are calculated and perpetuity value of company (the long term value of the company assuming steady flow of cash) is taken into account by using the growth factor on the 3rd year cash flow of the company and extrapolating with the discount factor (see the formula below). The valuation of the company is calculated by adding 5 year discounted cash-flow with the perpetuity value.

Venture Capital Method

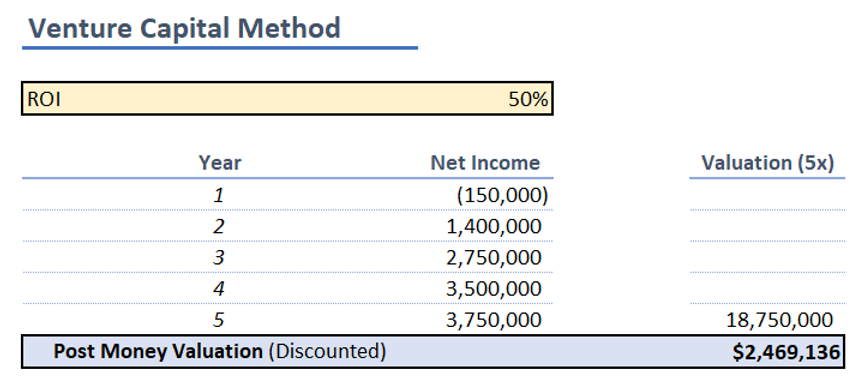

The Venture Capital method is mostly used for establishing a mathematical valuation even without current revenue. Investors set the expected exit valuation and how much return they are expecting to generate (most of the time the VCs have a minimum ROI rate; thus if you can anticipate the future value of your company you can calculate the current valuation). From thereon you can calculate your post money and pre money valuation with the ticket size.

In the example below you may see a scenario for an investment with exit at the end of year 5. The start-up is expected to have a net income of 3.75M USD by year 5 and the comparable companies are valued at a ratio of 5xNet Income. This brings the valuation of company at 18.75M USD which is discounted to ~2.5M USD thus the post money valuation of the company is at 2.5M USD. For this example if 500kUSD is invested in this start-up with this valuation the VC acquires 20% of the start-up, if everything goes according to the plan the 20% would be valued at** 3.75M USD** giving a **7.5x **return on their investment.

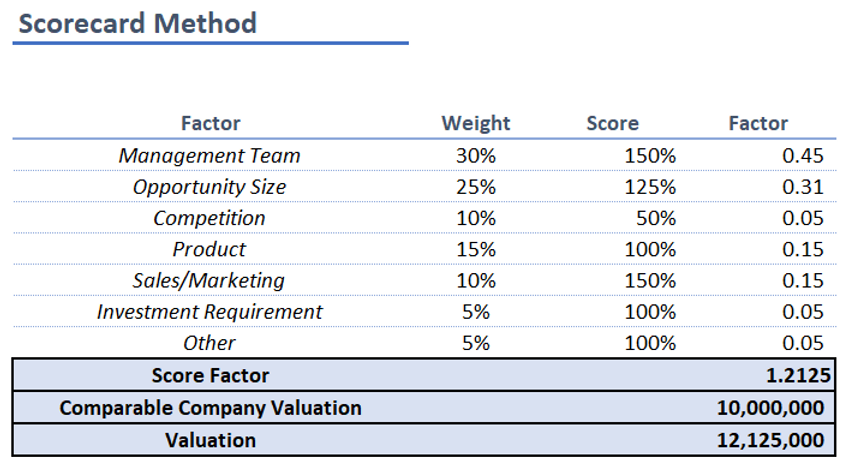

Scorecard Method

The Scorecard method is an ideal valuation method for pre-revenue companies. As creating projections without any actual revenue would be a vain effort; for the scorecard method you select a comparable company valuation (or median of several companies); then you score your company and you determine the factors affecting the valuation.

The factors may that can be scored are :

-

The management team (experience, previous start-ups etc..)

-

Opportunity Size (the size of market potential)

-

Competition (how many competitors are already active, if there is an early mover advantage)

-

Product/Technology/IP (how unique, developed is the technology, if IP can be protected from competitors etc..)

-

Sales/Marketing (if there any active sales/marketing channels, potential partnerships)

-

Additional Investment Requirement (if the company will require more funding during scale-up)

-

Other (Any other factors such as hiring capabilities, access to key people or marketing activities, etc..)

You give a weight to each of these factors and you multiply your final score with the comparable company valuation to determine your company valuation.

In the below example an early start-up with a great product and team sees that a similar company in their field has been valued at 10M USD, they use the scorecard method to estimate their strength against the other company and determine their final valuation at 12M USD.

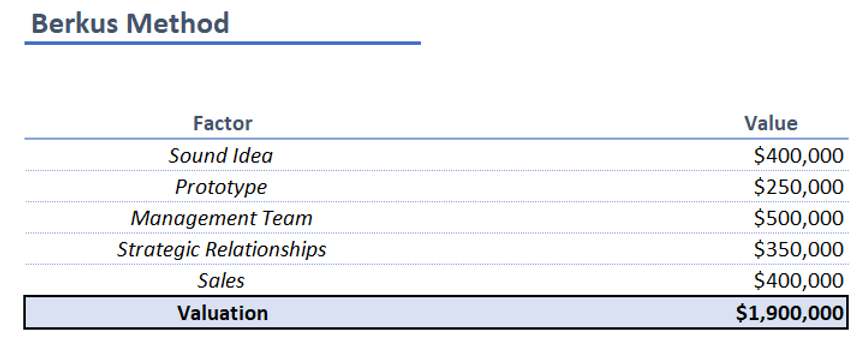

Berkus Valuation Method

The Berkus Method, similar to Scorecard method but focusing more on potential risks, evaluates certain factors of a start-up to determine the valuation. The method is applicable to pre-revenue companies as also noted by the developer of the method Dave Berkus (https://berkonomics.com/?p=2752)

“Once a company is in revenues, the Method is no longer applicable, as most everyone will use actual revenues to project value over time.”

The Berkus method 500k$ to 5 factors determining the value of a company ;

-

Sound idea (basic value)

-

Prototype (technology risk)

-

Management team (execution risk)

-

Strategic relationships (marketing risk)

-

Product Rollout / Sales (production risk)

Each of these factors are given 0-500k$ based on how developed your company is in each of the items. The creator of the method also states that in the current VC environment the method may have shortcomings to value the potential of a company considering that even a perfect score in each item would value your company at 2.5M$ and there are many start-ups funded with higher valuation pre-revenue.

Conclusion

To conclude, there are a few key concepts to keep in mind when valuing your start-up. First, make sure you have a clear understanding of your sector and the market you’re operating in. Second, ensure that you have a solid business plan and financials. And finally, don’t be afraid to get an expert opinion. If you are unsure of the value of your own company, contact us for a professional opinion.